Wage Woes

Wage Woes

Unemployment is at its lowest since 1969, yet the average American worker remains badly underpaid. Why?

Last month the national unemployment rate fell to 3.7 percent—a low it had not reached since October 1969, two months after Neil Armstrong set foot on the moon. Both conventional wisdom and historical experience would suggest that a tighter labor market—especially after the glacial recovery from the Great Recession—would bring robust gains for U.S. workers. No such luck.

By any measure, wages have remained stubbornly stagnant. From the onset of the recession through 2012, wages fell for the entire bottom 70 percent of the labor market. The Economic Policy Institute’s nominal wage tracker, which traces the annual change in private-sector nominal average hourly earnings (the current month compares to the same month a year ago), did not crack 3 percent until October 2018—nine years and fourth months after the “recovery” began. The Atlanta Federal Reserve’s wage growth tracker, a three-month moving average of median wage growth, has yet to top 4 percent—a dismal record that holds across regions, industries, occupations, age, and educational attainment.

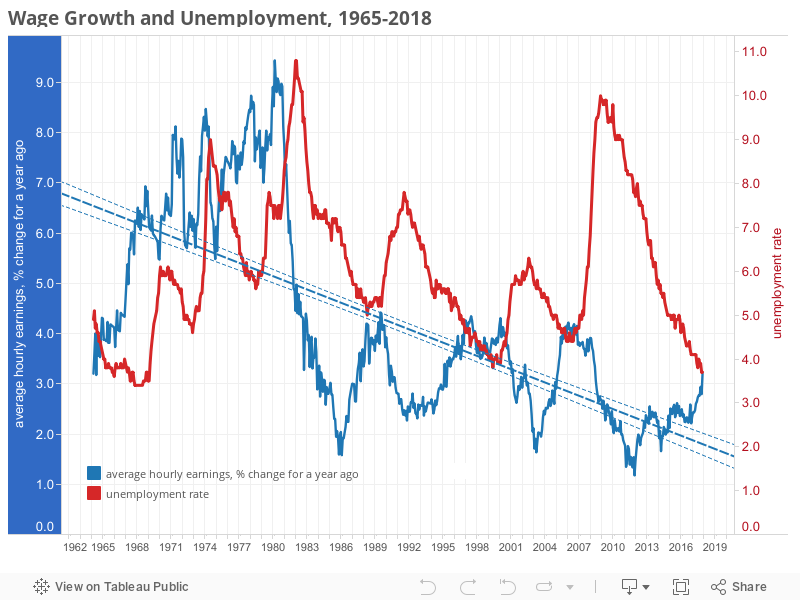

The line graph below traces wage growth (the percentage change in average hourly earnings over the last year) against the unemployment rate. Unsurprisingly, across this span, as unemployment rises wage growth falls off, and as the employment situation improves wage growth soon follows. But the downward trend in wage growth (the dotted blue line) underscores the key concern: with each successive business cycle, wages are slower and slower to recover.

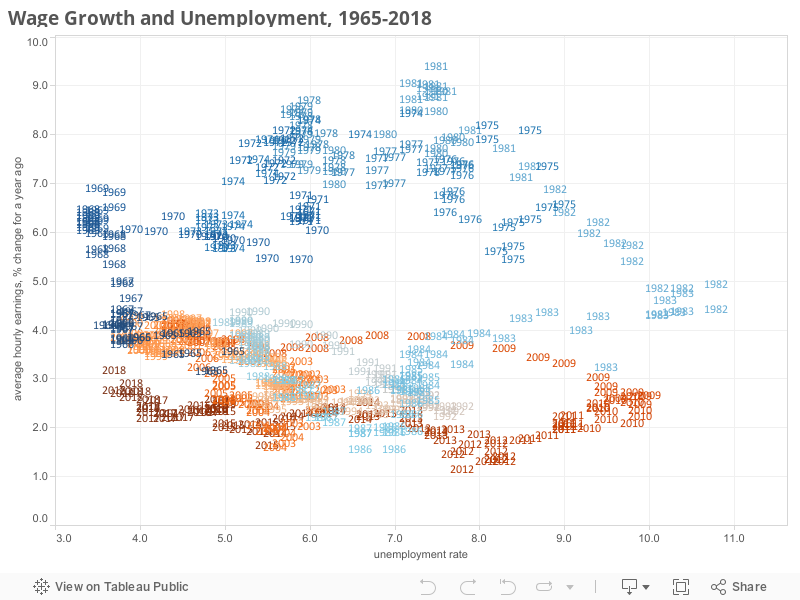

Another way to look at this is to plot the relationship between the unemployment rate and wage growth, month by month, for the same span. In this graph, each year is represented by twelve plotted months (labeled by years—scroll over to see the month); the months are shaded from blue (earliest) to red (most recent). Here the dismal wage record of the Great Recession and recovery is starkly evident. The plots representing the last ten years crowd the bottom of the graph, indicating sluggish wage growth across the last business cycle.

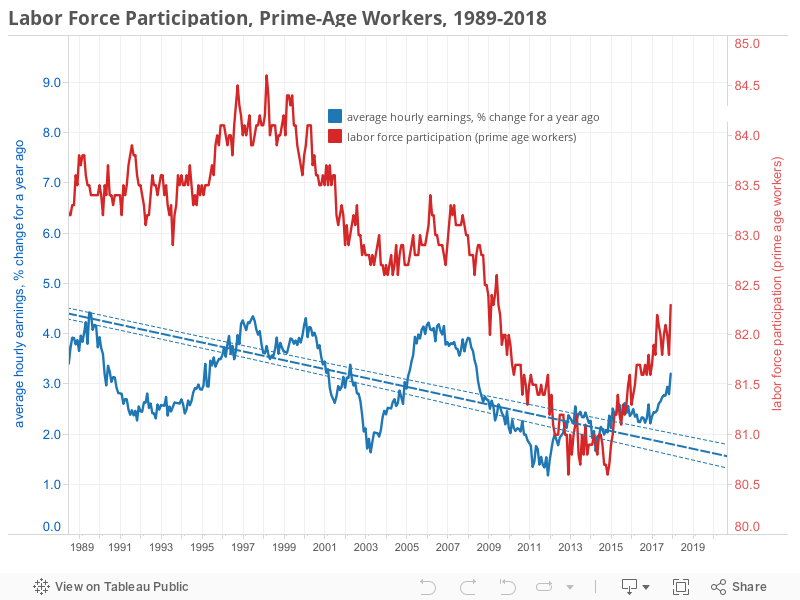

There are a number of potential culprits in this story. One possibility is that there is still a lot of slack in the labor market—that this is not your father’s 3.7 percent unemployment rate. The Great Recession generated not just unemployment but significant underemployment—including those who have given up looking for work (and hence were not added to either the numerator or the denominator of the conventional unemployment rate), and those working part time who would prefer full-time work. Indeed, one lingering hangover from the Great Recession is a sustained bump in the number of prime-age workers who have left the labor force entirely. Underemployment can be just as important a drag on wages as unemployment. Indeed, as the figure below suggests, the decline in labor force participation tracks wage stagnation pretty closely.

Another possible culprit is the slow growth in labor productivity, which, as then–Fed Chair Janet Yellen warned in 2016, “has been unusually weak in recent years.” Most of the economic growth across the recovery has come from an increase in the hours worked rather than increases in productivity (the output per hour worked). Some economists see this stagnation as a lasting problem, arguing that nothing on the horizon promises to match the dramatic productivity gains of the twentieth century. Others counter that the gains of the “information age” have yet to be fully realized, or that our measure of labor productivity is failing to capture the efficient ways we now consume goods and services (one-click ordering, same-day shipping, instant price comparison across sellers) .

But these internecine debates miss the point. Even if labor productivity were magically to double, there is no reason to assume the gains would show up on paychecks. As the Economic Policy Institute has tirelessly documented, productivity growth was broadly shared in the first generation after the Second World War, when both the size of the economy and the real (inflation-adjusted) compensation of workers nearly doubled. Since the early 1970s, productivity is up another 77 percent while real wages have gone up just 12 percent. Across this same era, educational attainment improved dramatically: between 1975 and 2017, the share of Americans twenty-five and over with a high-school degree or better increased from 62.5 to 89.6 percent; the share with a bachelor’s degree or better increased from 13.9 to 34.2 percent. It is not the health of the economy, in other words, that has battered workers and dampened wage growth, but a dramatic and sustained change in the distribution of its rewards.

What’s flattening wage growth—and hammering in that wedge between pay and productivity—is the continuing collapse of the bargaining power of U.S. workers.

This reflects, in part, longstanding occupational shifts which have polarized opportunity. One in four U.S. workers labor in low-wage jobs (those paying less than two-thirds of the median wage)—easily the highest rate among our democratic and economically developed peers, and a rate that is growing. Since 2007, the lion’s share of new jobs have been in lower-wage occupations than those lost during the preceding recession. And projections of future job growth are heavily skewed toward low-wage service occupations.

But, more important, compensation and job quality have deteriorated across the occupational spectrum. The “low-wage” in “low-wage jobs,” after all, is a reflection not of market-value but of the abysmal state of U.S. labor standards—including a minimum wage that leaves a single working parent with one child below the poverty line, hours and schedules that play havoc with work-life balance, a “private welfare state” of pension and health coverage that dramatically widens the gap between good jobs and bad jobs, and an indifference to enforcement that leaves working Americans—especially the most vulnerable—at risk of wage theft.

Into the late 1970s, organized labor had the power to raise wages for members and non-members alike, to insulate paychecks from recessionary spikes in unemployment, and to narrow wage and income inequality. But for workers across the bottom two-thirds of the earnings distribution today, the benefits of collective bargaining—for union workers, for non-union workers, and for women—have virtually evaporated. Private-sector union membership is now under 6 percent of the workforce. And public-sector unions, in the wake of concerted attacks at the state level and the Supreme Court’s Janus decision, are losing members (since the passage of Bill 10 in Wisconsin in 2011, public-sector union membership in the state has fallen from 40 percent to under 20 percent) and losing bargaining power even where they maintain membership.

The peril for working Americans is magnified by the fact that, as their individual or collective ability to win better wages has eroded, their employers have amassed greater and greater economic and political clout. Labor’s share of national income has fallen almost 13 percent since 2000. Local labor market concentration (including the domination of wage-setting behemoths like Amazon or Walmart) allows employers to set (or strangle) local wages, dampening wage growth in good times and bad. This market clout is exaggerated in rural settings where a single employer—a mine, a packing plant, a big-box retailer—often dominates the labor market.

This starkly unequal distribution of rewards—and its political roots—can be seen in cartoon form in the first year of the Trump tax cuts. In November 2017, Trump claimed he was “slashing business taxes so employers can create jobs, raise wages, and dominate their competition around the world.” By November 2018, the distributional silliness of this claim was painfully apparent. The tax cuts, by intent and design, overwhelmingly went to high earners and corporate profits. The corporate windfall was largely invested in stock buybacks—pumping up share value and executive pay at the expense of wage gains.

Shared prosperity, including the expectation of wage gains in the long recovery from the Great Recession, rests on policies and institutions that sustain the bargaining power of workers. In the absence of such policies and institutions, even exceptional stretches of near-full employment may not be able to interrupt persistent wage stagnation, rising income inequality, and growing economic insecurity.

Persistent structural forces—wage inequality; weak worker bargaining power; a deeply ingrained reluctance among powerful employers to share the benefits of productivity growth with middle-wage workers; politics hostile to workers, unions, and labor standards—are all pushing hard the other way. Until there’s a countervailing force, productivity growth and the pay of too many workers will continue to diverge.

Colin Gordon is a professor of history at the University of Iowa. He writes widely on the history of American public policy and is the author, most recently, of Growing Apart: A Political History of American Inequality and Citizen Brown: Race, Democracy, and Inequality in the St. Louis Suburbs (forthcoming, University of Chicago Press).