The Pension Pinch

The Pension Pinch

A new survey reveals just how severely the United States’ pension system is failing its retirees.

The American system of retirement famously rests on three legs: personal savings and assets, employment-based pensions, and Social Security. Like any tripod, the system is efficiently stable when all three legs are strong, but also vulnerable to weakness in any one of them. Over the last generation, a combination of wage stagnation, declining job quality, and recessionary damage has chiseled away at family resources and job-based benefits. The malevolent misdirection of market fundamentalism, of course, is to sharpen its saws for Social Security—the only leg of this stool still bearing any weight.

Family savings—including not just retirement savings but also other asset cushions like home ownership—are increasingly shaky. The personal savings rate, which hovered at or above 10 percent from the 1960s to the mid-1980s, is now a meager 4.8 percent. According to a recent survey by the National Institute on Retirement Security, 45 percent of working-age Americans have no retirement account assets, 62 percent of near-retirement households (ages 55-64) have retirement savings that amount to less than a year of annual income, and the median retirement savings for those households is a paltry $14,500. These numbers, not surprisingly, are also sharply skewed by race, income, and educational attainment.

So what about job-based pensions? Our retirement system (like out health care system) is premised on the notion that public policy need only mop up around the edges, or supplement, employment-based plans. But private pension coverage grew modestly through the middle years of the last century and plateaued at only about half of the workforce. Coverage at work was a sort of lottery, largely dependent on job characteristics like industry, firm size, and union coverage. And such coverage widened labor-market inequalities, as pension plans followed high wages and job tenure.

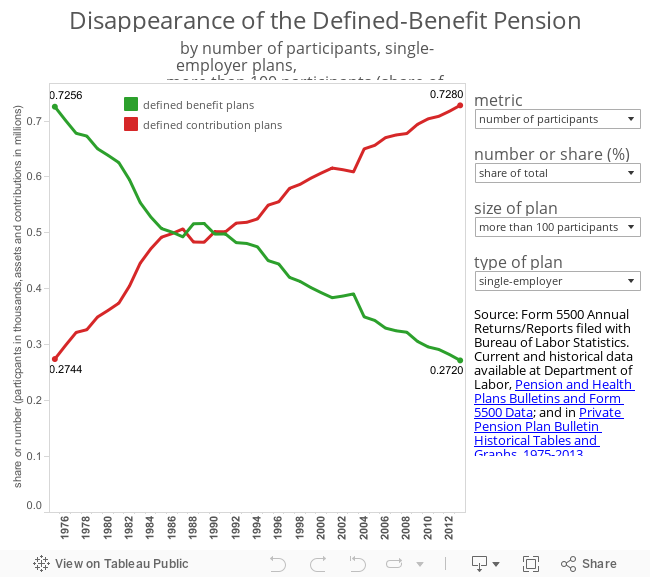

But even for those workers claiming coverage, retirement security has been whittled away. The private pension of the last generation was usually a defined-benefit plan, financed largely (often wholly) by the employer, and promising a lifetime annuity based on years of service and earnings. Most coverage today takes the form of a defined-contribution plan, such as a 401(k), to which the worker is often the only contributor, and whose retirement benefits depend (often disastrously) on the performance of private equity or company stock. The graphic below captures to slow displacement of defined-benefit pensions, by number of plans, number of participants, contributions, assets, and benefits.

A retirement system should both facilitate savings, managing the risk of retirement across a lifespan, and even out some of the inequality generated by the market, managing the risk of retirement across a diverse population. Our public-private hybrid accomplishes neither. Personal retirement savings and job-based coverage masquerade as private achievements, but depend heavily on the tax advantages that accrue to both; indeed the exclusion of pension contributions and earnings represents a tax expenditure of over 1 percent of GDP, in the range of $1.7 trillion. By the same token, Social Security benefits are shaped largely by private employment and earnings history; the benefit structure softens market inequities but also sustains them. Our public-private social insurance system is an artifact of patterns of employment and labor force participation that are no longer with us. What was once a source of security (at least for many) is now just another eddy of inequality, eroding retirement savings at one bank of the income stream and depositing them at the other.

Although the retirement security crisis is dire, the solutions are well within reach. One tack would be to further encourage, subsidize, or mandate job-based pension savings. This could be accomplished by making it easier for small businesses (very few of whom offer pensions) to establish plans; or by mandating modest retirement plans (jointly financed, conservatively-invested) for all workers—with a refundable tax credit to make the plans accessible to part-time and low-wage workers. Another tack would be to decouple retirement security from work. The Obama administration’s recently launched myRA program (which features no minimum deposit, no fees, and a modest return backed by Treasury bonds) takes a step in this direction—although low-income workers are unlikely to claim the tax advantages, and there is no mechanism for employer contributions. And, of course, any of this should be accompanied by recommitting to Social Security, ensuring its future by raising (or removing) the cap on taxed earnings, and nudging the payroll tax rate up 2 or 3 percent. But try telling that to Paul Ryan.

Colin Gordon is a professor of history at the University of Iowa. He writes widely on the history of American public policy and is the author, most recently, of Growing Apart: A Political History of American Inequality.