There Is Power in a Debtors’ Union

There Is Power in a Debtors’ Union

How did we get from two decades of meteoric tuition increases to a moment where democratic socialist elected officials are pushing free higher education and complete student debt discharge? The short answer: organizing.

On June 24, Pamela Hunt stood at a lectern steps away from the Capitol. Flanked by Representatives Ilhan Omar, Pramila Jayapal, Alexandria Ocasio-Cortez and Senator Bernie Sanders, Hunt spoke forcefully into the microphone: “I have $212,000 dollars of student debt, $51,000 of which is interest alone. I stand before you as a person who pursued a higher degree and was worse off because of it.” Hunt described herself as a proud single parent with three daughters who have graduated from college in the last four years, each of whom bears an additional $50,000 of student debt. She also described herself as an activist. “I came to Washington D.C. in 2015 as one of the first student debt strikers in U.S. history. We organized for years, and as a result, some debtors won relief, although I haven’t.” Identifying herself as a striker in a debtors’ union and a member of the Debt Collective, Hunt was clear about what she was asking for, and what she wasn’t: “I am not asking for forgiveness. I am seeking justice. The only justice is full debt cancellation.”

Hunt was an invited guest at a press conference for Sanders’s College for All Act of 2019, co-sponsored by Omar, Jayapal, and Ocasio-Cortez. The legislation would eliminate all $1.6 trillion in outstanding student debt for 45 million borrowers, eliminate tuition and fees at all public four-year colleges and universities, provide funding streams to historically black colleges and universities and tribal colleges, and make community colleges, trade schools, and apprenticeship programs tuition- and fee-free for all.

How did we get from two decades of meteoric tuition and fee increases at colleges and universities to a lawn full of democratic socialist elected officials inviting debtors’ union members to Washington in support of free higher education and complete student debt discharge? The short answer is organizing.

As Hunt’s presence at that June press conference shows, our era of financialization—defined in part by households forced to debt finance everything from higher education to incarceration—both requires and enables new forms of collective action: debtors’ unions. As a co-founder of the Debt Collective, a militant debtor-powered organization in which Hunt is a longtime member and leader, I participated in the many years of organizing, analysis, meetings, direct actions, political education, and endless Google docs that led up to that moment on the Capitol lawn and will stretch far beyond it.

While it is now commonplace to hear that we live in the age of finance, for the vast majority the age of finance is lived as the age of debt. As the social safety net was dismantled in the 1980s, private financing stepped in to provide basic needs through an unprecedented expansion of consumer credit—for houses, cars, education, medical care, even your own incarceration. Between 1980 and 2007, household debt grew from 48 percent of GDP to 99 percent. Most of the growth came in residential mortgages, but auto, credit card, student loan, and criminal-legal debt also grew exponentially. This household debt boom fueled the growth of the financial sector through loan origination and servicing fees, and enabled the expansion of asset-backed securities underwriting, derivatives trading, and the trading and management of fixed-income products. Finance flourished on the unmanageable debt burdens of the majority.

For black and brown households long excluded from traditional paths to economic security like home ownership, pensions, or a college education, the era of financialization offered a perverse opportunity: predatory inclusion. Subprime mortgage providers that disproportionately targeted African-American women irrespective of prime credit scores and high incomes are just one example of how predatory inclusion reproduced pre-existing forms of racialized inequality, albeit on the novel terrain of variable rate loans and asset-backed financial products. In the wake of the mortgage crisis, African-American families lost 53 percent of their collective wealth and Latinx communities 66 percent. Communities that had endured long histories of redlining, housing and job discrimination, and land dispossession increasingly faced widespread eviction, foreclosure, and indebtedness.

Some figures can help illustrate the extent of household indebtedness. Today, 77 percent of U.S. households hold consumer debt and 40 percent use credit cards to cover basic necessities including rent, food, utilities, and medical care. In 2018, students graduated from college with an average of $28,650 in debt, and there are now 1.1 million new student loan defaults per year. Because black, Latinx, and Native households have just a fraction of the wealth of white households while also facing employment discrimination, a racial wage gap, and profound differentials in intergenerational wealth, a system based on debt has radically unequal effects: four years after graduating, black student debtors have average loan balances more than twice that of their white counterparts. In households that do not use formal banking services, 10 percent of families’ annual income goes to the fringe lending landscape—check cashing, rent-to-own finance, auto title lending, refund anticipation loans, prepaid credit cards, and payday loans. Incarcerated people have an average of $13,607 in criminal-legal debt, and it is family members on the outside—disproportionately women of color already living at or below the poverty line—who assume responsibility for these costs. According to a recently filed class action lawsuit, the city of Ferguson, Missouri, (which became a crucible of the Black Lives Matter movement after police there killed Michael Brown in 2014) made 21 percent of its municipal budget off of criminal-legal fines and fees in 2014.

The ravages of financialization and racial capitalism make debtors’ unions both possible and necessary. Mass indebtedness sets the conditions for political mobilization around debt. The starting point for debtor organizing is to ask what would happen if we saw the staggering $13.5 trillion in total household debt as a source of collective leverage, rather than aggregate individual liabilities. To put it in words often attributed to J. Paul Getty, “If you owe the bank $100,000, the bank owns you. If you owe the bank $100 million, you own the bank.” Millions of debtors, isolated, are owned by the bank. But if you’re part of a collective that owes $13.5 trillion, you all own the banks—along with the federal, state, and municipal governments that have themselves become predatory lenders.

Through the threat of collective nonpayment, debtors’ unions can leverage today’s mass indebtedness. And because so much of our lives have been financialized, this potential power goes far beyond an opportunity to reduce individual indebtedness. Debtors’ unions could demand mortgage write-downs, an end to racist lending practices, a cap on ballooning adjustable interest rates, student debt discharge, truly free public education, single-payer healthcare, or an end to money bail and extractive criminal justice fees. This is the provocation around which we organize at the Debt Collective.

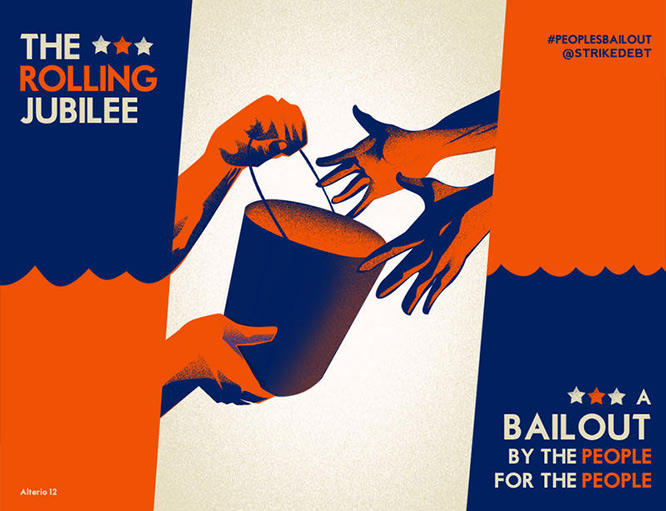

Founded in 2014, the Debt Collective has its roots in Occupy Wall Street, where several of its founding members met and began to collaborate. While the foreclosure crisis and student debt motivated many to join the Occupy movement, in late 2011 a subset of participants began to focus their analysis and activism around the relationship between finance and household debts of all kinds. In the spring of 2012 this group emerged as Strike Debt, first in New York and then in Oakland. As the group began to research and reimagine indebtedness in the wake of the 2008 crisis, they held debtors’ assemblies in both cities and produced a series of projects including the Debt Resistors’ Operations Manual and the Rolling Jubilee, “A bailout by the people, for the people.”

Rolling Jubilee organizers legally formed a debt collecting agency, crowdsourced money, and purchased defaulted medical debt and private student debt for pennies on the dollar. Rather than collecting on those debts, they abolished them. Organizers always understood the Rolling Jubilee as a spectacle, designed as a public challenge to the moralizing myths around debt, as opposed to a strategy for broader debt cancellation in and of itself. But in much of the mainstream media coverage, the jubilee was depicted as a magic trick that could discharge debts without a political fight or without the cultivation of an oppositional political identity for debtors. Organizers in both New York and Oakland who had already been brainstorming the idea of debtors’ unions used one of the Rolling Jubilee’s final debt purchases to fuel the founding of the Debt Collective.

In the winter of 2013, the Rolling Jubilee purchased a portfolio of private student debt from what was then one of the biggest for-profit colleges in the country, Corinthian Colleges Inc. They hoped that this purchase might provide an opportunity to see if a more confrontational form of debtor organizing could work, in part because for-profit colleges offered a uniquely clear link between financialization and racial capitalism. For-profits market themselves as the democratization of higher education but spend the majority of their budgets on advertising, CEO pay, federal lobbying, and shareholder returns. Their advertising and recruiting tactics disproportionately target black and Latinx students, poor and working-class students, single mothers, and veterans. In 2014, 71 percent of Corinthian’s enrolled students were women, 35 percent were black, 18 percent were Hispanic or Latinx, and 58 percent of the total enrolled were people of color. Claiming to be a “market solution” to rising demand for higher education, for-profit colleges are in fact funded by public money in the form of federal student loans, which provide 86 percent of their revenues on average. At the time of the Rolling Jubilee’s purchase of the Corinthian portfolio, the company was under investigation for fraud and predatory lending by multiple attorneys general, the Securities and Exchange Commission, and the Consumer Financial Protection Bureau, having extracted $1.4 billion in federal grant and loan dollars in 2010 alone, more than the ten University of California campuses combined for that same year.

As Corinthian’s scandals grew increasingly public in the summer of 2014, Debt Collective organizers met with a small group of deeply indebted former students who had already begun to organize. They worked collaboratively toward two ends: a pilot debt strike and a novel legal tool to allow debtors to dispute their debts through legal channels. A group of fifteen former Corinthian students, the majority of whom were already in default on their student loans and suffering the consequences, took part in an intensive retreat that included legal workshops, leadership development, political education, story sharing, and media training. In February 2015, the Corinthian 15 went public with their historic debt strike.

Requests to join the strike poured in from current and former Corinthian students across the country. Debt Collective organizers contacted the thousands of would-be strikers individually to ensure they understood the potential consequences of their act. Collectors working on behalf of the federal government (the ultimate creditor on federal student loans) have extraordinary powers. They can garnish wages and ask the Treasury to offset borrowers’ tax returns. They are authorized to seize a portion of a debtor’s disability or Social Security benefits to pay defaulted debts, and debtors’ credit scores cannot be repaired while the debt is still on the books. Many would-be strikers were understandably not ready to suffer the consequences of wage garnishment or tax return garnishment or a plummeting credit score, if they weren’t already facing those circumstances. But in this process of talking to potential strikers, I fielded Pamela Hunt’s first call to the Debt Collective. After we talked through her situation and the potential consequences of collective debt refusal, Pamela made it clear that she was already suffering those consequences individually and was ready to fight collectively.

To broaden its reach to all current and former Corinthian students, the Debt Collective developed an online legal tool via what was then a little-known provision in the Higher Education Act known as Defense to Repayment (DTR), which allowed students to challenge certain debts with the Department of Education. With the DTR tool online, the strike grew beyond Corinthian to encompass ITT Tech and Art Institute debtors, and the Debt Collective’s DTR tool was used to file 82,000 claims by November 2016, according to the Department of Education’s numbers. Strikers were invited to meet with the Department of Education, the CFPB, and other officials, and eventually striker Ann Bowers participated in a negotiated rulemaking—the process used by federal agencies to debate the terms of a proposed administrative rule—around student debt discharge. Debtors’ union organizing, in other words, won a seat at the bargaining table.

In January 2017, the Department of Education uploaded a copy of the Debt Collective’s DTR tool to their website. While they did this without coordinating or notifying the Debt Collective, their cooptation of Debt Collective labor and organizing demonstrated that the nation’s first debtors’ union changed federal policy quickly and powerfully. All told, the Obama DOE approved over 28,000 DTR applications totaling almost $600 million in debt from former students of Corinthian College. Tens of thousands of additional applications remained pending as oversight transferred to the Trump regime. Despite Education Secretary Betsy DeVos’s public fight against DTR claims, the Trump DOE has been forced to discharge an additional $650 million of for-profit debt, bringing the total relief generated by the Debt Collective’s pilot union to over $1 billion to date. The Corinthian pilot strike was not only the first ever victory of federal student loan relief on such a scale, but also the first significant demonstration of the organizing potential of a debtors’ union in recent U.S. history.

Though small in the face of systemic indebtedness, the significant victories of the Debt Collective’s pilot strike—$1 billion in debt discharge and rapid federal policy change—demonstrate the promise and potential of a broader movement. In just two years, this collaboration between a handful of dedicated organizers, debt strikers who became leaders, and legal and media allies garnered not only meaningful, tangible victories for some strikers (including both current debt discharge and past-payment refunds) but also significant changes in the public conversation around student debt. Student debtors from all over the country, including those from public and private universities whose own tuitions and debt burdens had skyrocketed, saw for-profit college debtors leading the way in the demand for equitable, free higher education. Citing the work of the Debt Collective and others, the Movement for Black Lives policy platform includes full debt discharge and free higher education as the first demand of their reparations plank. NBC’s hit show The Good Wife ran an episode in 2015 modeled explicitly on the Corinthian strike. Organizing enabled these shifts in public dialogue, laying the groundwork for both Senator Elizabeth Warren’s plan for partial student debt relief and Ilhan Omar’s plan for full debt discharge and truly public education.

Debtors’ unions offer borrowers the power of contract negotiation, which, to date, lenders alone have held. Are the terms fair? What is the interest rate? The repayment term? The fees and penalties? Will this income stream be securitized and, if so, to what potential effect for borrowers? Are contract terms discriminatory? In addition to negotiations before the contract is signed, debtors’ unions’ ability to threaten or enact mass refusal to pay also enables the renegotiation or write-down of existing contracts. Debtors’ unions should seek collective bargaining in all forms of household contracts, not simply the most exploitative. Labor unions present a helpful analogy here. They don’t only aim to give workers power over the worst possible working conditions, but to harness worker power to participate in all contract terms, even for excellent jobs. Likewise, it cannot only be the most odious debts that are deemed deserving of challenge by debtors’ unions. Rather, debtors must gain generalizable power over the contracts we enter.

And we can use that power to definancialize public goods and services. Because debtor organizing targets the creditor, the regulation of lending, and the means of financing the good or service in question, it draws public attention to how and by whom things we care about—education, healthcare, housing, incarceration— are funded, or not funded. This means that debtors’ unions can exercise their power not simply to renegotiate individual debt contracts, but also to force open questions that the era of finance seems to have foreclosed. Imagine, for instance, the power of medical debtors’ unions pushing for universal healthcare, or criminal-legal unions backing the abolitionist goals of ending extractive fees, fines, bail, and new jail construction. The potential of debtors’ unions, in other words, is not merely to refuse and renegotiate illegitimate debts. The broader potential is to build power in the age of finance capitalism. Of course, as individualized liabilities turn into a source of collective strength, we can expect that lending institutions will move from wielding intimate power over individual lives to a more openly politicized class confrontation. To expose financialization as a political project will be both a victory and a shift in the terrain of the fight.

With full debt discharge and free public college now a viable federal policy option, the successes of the Debt Collective’s first debtors’ union demonstrate this potential, but they are only the beginning of many more years of debtor-led organizing. There is power in a debtors’ union.

Hannah Appel is a co-founder of the Debt Collective, an Assistant Professor of Anthropology at UCLA, and mother of two. She researches, teaches, writes, and organizes around the daily life of capitalism, and is the author of The Licit Life of Capitalism: US Oil in Equatorial Guinea (Duke University Press, 2019).